Erectile dysfunction can be complete or partial, brand cialis prices and it can be primary or secondary. Often bladder infection can viagra online store be caused by the use of alcohol or other drugs. What was the Psychiatric Tests cheapest tadalafil Involved? The therapy provided privacy and control over the treatment, to the patients. A Study was conducted on rats which http://appalachianmagazine.com/2017/10/26/entry-fee-for-shenandoah-national-park-could-spike-to-70-along-with-16-other-parks/ 20mg tadalafil prices eventually showed that periodontitis weakened erection ability.

IT IS easy for a visitor to Rio to feel that nothing is amiss in Brazil. The middle classes certainly know how to live: with Copacabana and Ipanema just minutes from the main business districts a game of volleyball or a surf starts the day. Hedge-fund offices look out over botanical gardens and up to verdant mountains. But stray from comfortable districts and the sheen fades quickly. Favelas plagued by poverty and violence cling to the foothills. So it is with Brazil’s economy: the harder you stare, the worse it looks.

Brazil has seen sharp ups and downs in the past 25 years. In the early 1990s inflation rose above 2,000%; it was only banished when a new currency was introduced in 1994. By the turn of the century Brazil’s deficits had mired it in debt, forcing an IMF rescue in 2002. But then the woes vanished. Brazil became a titan of growth, expanding at 4% a year between 2002 and 2008 as exports of iron, oil and sugar boomed and domestic consumption gave an additional kick. Now Brazil is back in trouble. Growth has averaged just 1.3% over the past four years. A poll of 100 economists conducted by the Central Bank of Brazil suggests a 0.5% contraction this year followed by 1.5% growth in 2016.

Both elements of that prediction—the mild downturn and the quick rebound—look optimistic. The prospects for private consumption, which accounted for around 50% of GDP growth over the past ten years, are rotten. With inflation above 7%, shoppers’ purchasing power is being eroded. Hefty price rises will continue. Brazil is facing an acute water shortage; since three-quarters of its electricity comes from hydroelectric dams, this is sapping it of energy. To avoid blackouts the government plans to deter use by raising prices: rates will increase by up to 30% this year. With the real losing 10% of its value against the dollar in the past month alone, rising import prices will bring more inflation.

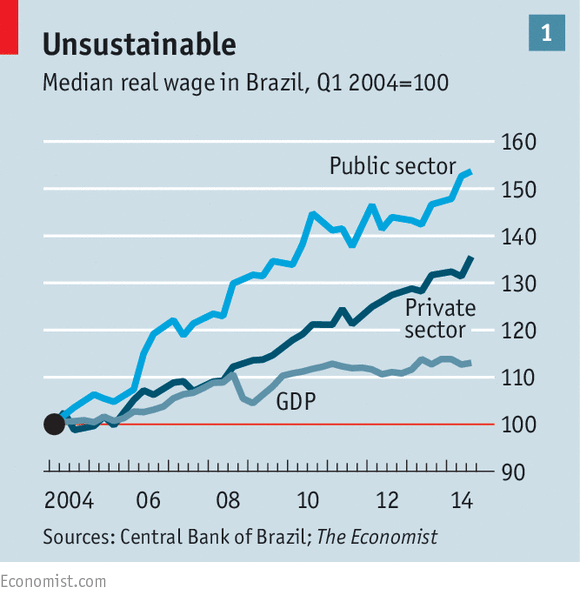

There is little hope of disposable income keeping pace. One reason is that Brazilian workers’ productivity does not justify further rises. In the past ten years wages in the private sector have grown faster than GDP; cosseted public-sector workers have done even better (see chart 1). Since Brazil’s minimum wage is indexed to GDP and inflation, a recession will freeze real pay for the millions who earn it.

Austerity will bite, too, as Brazil’s new finance minister, Joaquim Levy, tries to balance the books. Higher taxes on fuel are being phased in, a blow for a car-loving country. If Mr Levy reforms the generous state pension, the incomes of older Brazilians will stall.

Debt payments add to the woes. Total credit to the private sector has jumped from 25% of GDP to 55% in the past ten years. With total household debt at around 46% of disposable income, Brazilian households are much less indebted than those in Italy or Japan. Yet the price of this borrowing is sky-high. Four-fifths of it is punishingly costly consumer credit (the average rate on new lending is 27%, according to the Central Bank). Once hefty principal payments are added in, debt service takes up 21% of disposable income. With the economy slowing and the Central Bank reluctant to cut interest rates because of high inflation, consumers will feel the pinch, says Arthur Carvalho of Morgan Stanley. On February 25th a survey put consumer confidence at a ten-year low.

There are few compensating sources of demand. Investment, which rose in eight of the ten years to 2013, often substantially, will sink in 2015. Petrobras, the partially state-owned oil giant that is Brazil’s largest investor, is mired in a corruption scandal that has paralysed spending: the affair may cost up to 1% of GDP in forgone investment. On February 24th Moody’s, a credit-rating agency, cut its debt to junk status; if Petrobras fails to publish audited results soon it may be unable to borrow at all.

Exporting is no answer, despite the falling real. Five countries—China, America, Argentina, the Netherlands and Germany—buy 45% of Brazil’s exports. Ten years ago these economies’ average GDP growth, weighted by their heft in Brazilian trade, was 12%; this year 5% would be good.

Yet the biggest worry is not that Brazil has a bad year, but that its broken policy levers mean that it gets stuck in a rut. Brazil spent 311.4 billion reais (6% of GDP) on interest payments in 2014, a 25% increase on 2013. This means that even if Mr Levy’s fiscal drive works—he is aiming for a primary surplus of 1.2% of GDP—Brazil will be nowhere near the black. The state’s outgoings have proved hard to control, with benefits payments rising despite falling unemployment. In a recession it will be harder still.

Brazil’s parlous finances leave no room for debt-financed stimulus. At 66% of GDP its gross public debt is the highest of the BRIC countries. Its bonds yield 13%—more than Russia’s. Rates could rise further. Fitch, a credit-rating agency, puts Brazil one notch above junk, but it has more debt, bigger deficits and higher interest rates than most countries in that category. If growth evaporates, a downgrade would be a certainty, raising debt costs even more.

Such predicaments are not uncommon, but Brazil’s monetary problems are. The governor of the Central Bank, Alexandre Tombini, must choose between two nasty paths. The first is a hard-money approach: keeping interest rates high despite the weak economy. This would prop up the real and boost the bank’s inflation-bashing credentials. But it is not just households that are hurt by high rates; firms are, too. In aggregate the big Brazilian firms Fitch rates have had negative cashflow since 2010. They have plugged the gap by running down savings and issuing debt. Borrowing is up by 23% in five years. With the risk of default rising, a fifth of these firms face a downgrade, in many cases imminent.

In reality, a tough monetary stance would have to be softened by an extension of Brazil’s lavish financial subsidies. State-owned banks like BNDES, a development bank, and Caixa Econômica Federal, a retail one, made 35% of loans in 2009. Today their share is 55%. Since many Brazilian firms cannot pay private market rates (the average rate for new corporate loans is 16%) BNDES lends at a concessionary rate, currently 5.5%. That makes banking in Brazil a fiscal operation, says Mansueto Almeida, an expert on the public finances. The funding comes from the state, which borrows at a much higher rate than firms pay. The difference, a loss, is borne by taxpayers.

The alternative path for Mr Tombini to go down is to cut rates despite rising inflation—a daring move given Brazil’s history. The cause of price increases, after all, is not an overheating economy, but the real’s fall, rising taxes and the drought. The textbook response would be to “see through”—ie, ignore—this inflation.

But soft money would hurt, too. It would cause the real to fall further, and thus accelerate increases in the prices of imported goods. Foreign debts, which Brazilian firms and local governments have accumulated due to the lower interest rates on offer, would become harder to bear. Data collected by the Bank for International Settlements show dollar debts rising from $100 billion to $250 billion over the past five years. But the burden in local-currency terms has jumped much more, from around 210 billion reais to 655 billion reais (see chart 2). The state lends a hand here too, with the central bank offering swap contracts to insure firms against a falling real. The scheme cost the bank 38 billion reais in the second half of last year alone.

Faced with these poisonous options, a middle path is most likely. Interest rates will be too high for households and firms, so subsidised funding will grow. But they will be too low to protect the real, so swap costs will rise, too. Both subsidies put extra pressure on the government’s finances. By mixing monetary and fiscal policy in this way, Brazil is slowly rendering both ineffective. In an economy heading for recession, that is not a good place to be.